SEC Proposal Would Give Registered Funds Relief From Biden-Era Reporting Requirements

On February 18, 2026, the Securities and Exchange Commission proposed additional amendments to the reporting requirements on Form N-PORT for certain registered investment companies that will, if adopted, provide those funds with relief from existing requirements, as well as adding certain new reporting requirements.[1] The SEC is seeking public comments on the proposal, which will be due 60 days after publication in the Federal Register. The proposal would:

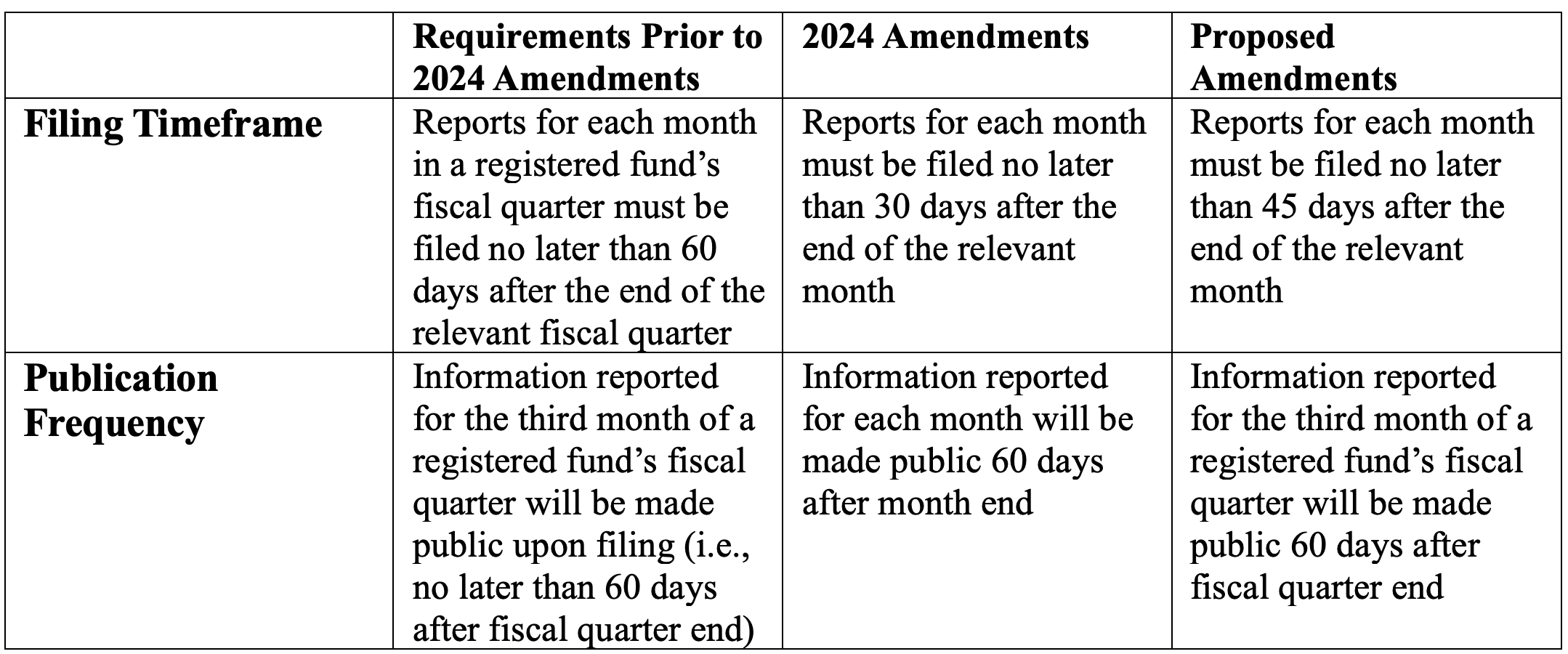

Require that monthly reports of portfolio-related information be filed within 45 days after month’s end, providing covered funds with an additional 15 days;

Reduce the frequency with which reports on fund holdings are published from monthly to quarterly;

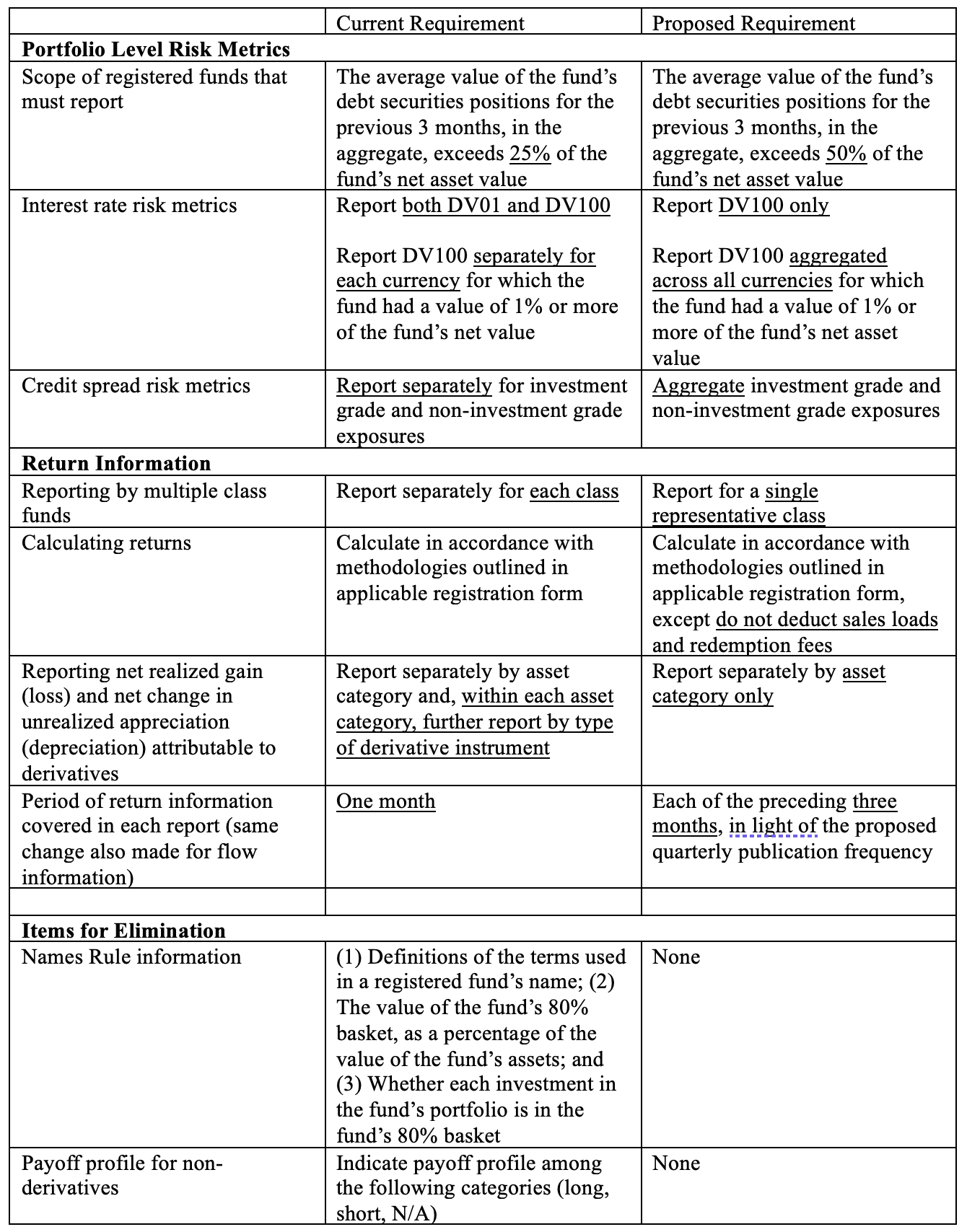

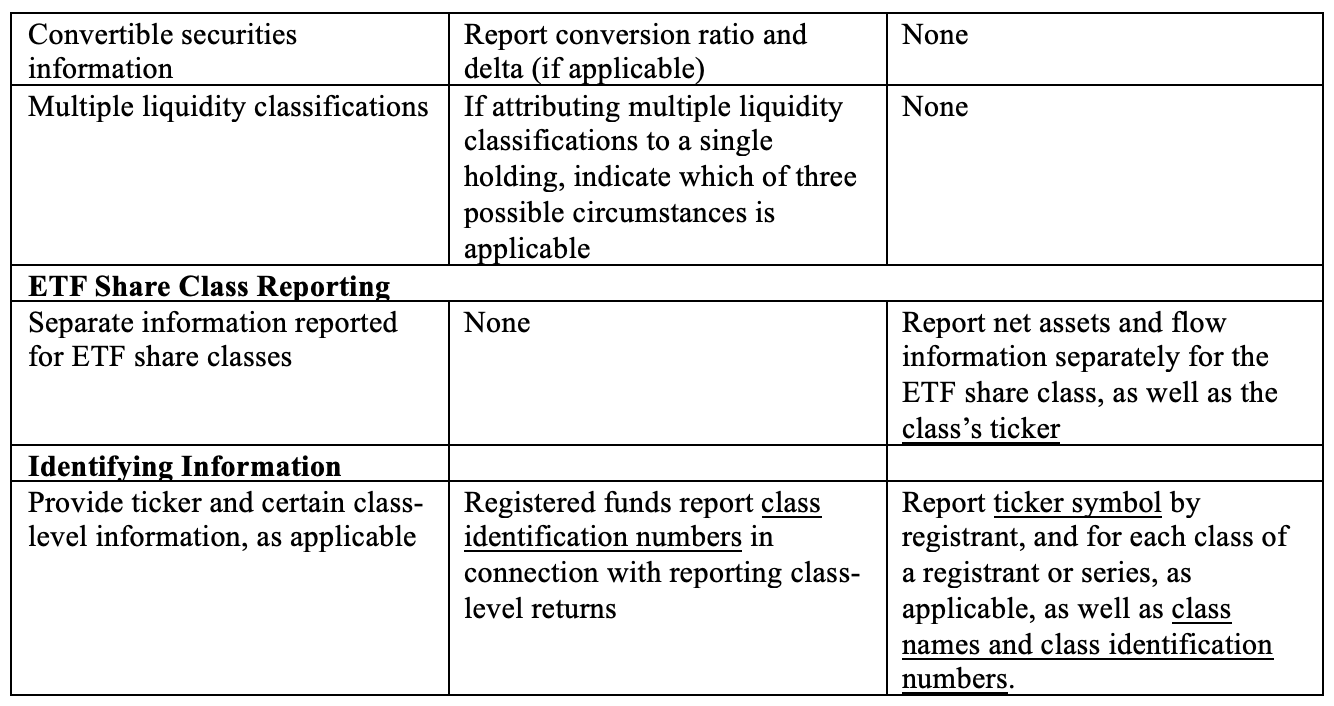

Streamline information collection on portfolio level risk metrics and returns;

Eliminate entirely certain reporting items, including requirements relating to the 2023 amendments to rule 35d-1 (the “Names Rule”);[2] and

Require certain additional information from funds, such as identifying information and information about funds with share classes that operate as exchange-traded funds.

Additionally, to allow the public time to comment on the proposed elimination of the reporting requirements relating to the Names Rule, the Commission has extended the compliance dates for those requirements.[3] These actions are the latest in a string of initiatives by the SEC indicating a renewed interest in engaging with the concerns of regulated funds and adopting a pragmatic approach to balancing regulatory burdens. We invite you to contact us if you would like any assistance or advice about engaging with the Commission.

Background

Registered management investment companies (other than money market funds and small business investment companies) and exchange-traded funds organized as unit investment trusts are currently required to periodically file reports on Form N-PORT to provide their monthly portfolio holdings and related information. During the previous administration, the SEC twice amended the reporting requirements under the form: in 2023, to add new reporting requirements relating to the Names Rule; and in 2024, to require more frequent filing and publication of these reports.

Funds expressed a variety of concerns with the amendments (e.g., increased compliance costs, risks of error, and frontrunning) and, in October 2024, a trade association brought suit before the Fifth Circuit Court of Appeals challenging the 2024 amendments.[4] Following the change in administration and in response to these concerns (as well as a Presidential Memorandum),[5] in the spring of 2025 the SEC announced it was extending the compliance dates for these amendments.[6]

Summary of Changes Under the Proposal

Comparison of Form N-PORT Filing and Publication Frequency Requirements Prior to the 2024 Amendments, the 2024 Amendments, and the Proposed Amendments

Comparison of Current and Proposed Reporting Requirements

Takeaways

The SEC has requested comments on the proposed amendments to Form N-PORT. Comments will be due 60 days after the proposal is published in the Federal Register. Additionally, the staff of the Division of Investment Management has prepared 2025-26 Names Rule FAQs, and identified certain Names Rule FAQs published in 2001 that it has determined should be withdrawn.

These developments are the most recent example that the Commission, the Division of Investment Management, and its staff, are willing to engage with the regulated community and are open to reconsidering existing regulatory requirements that may no longer make sense. We invite you to contact us if you would like any assistance or advice about engaging with the Commission.

If you have questions about this Client Alert or are interested in additional details or guidance, please reach out to Michael Khalil (michael.khalil@pierferd.com) or your regular PierFerd contact for assistance.

This publication and/or any linked publications herein do not constitute legal, accounting, or other professional advice or opinions on specific facts or matters and, accordingly, the author(s) and PierFerd assume no liability whatsoever in connection with its use. Pursuant to applicable rules of professional conduct, this publication may constitute Attorney Advertising. © 2026 Pierson Ferdinand LLP.

[1] See Form N-PORT Reporting, Investment Company Act Release No. 35962 (Feb. 18, 2026).

[2] The Names Rule requires certain funds to adopt a policy to invest at least 80% of the value of their assets in accordance with the investment focus that a fund’s name suggests. In 2023, the Commission adopted amendments to broaden the scope of this requirement to include, among other things, fund names that reference a thematic investment focus, including environmental, social, or governance (“ESG”)-related objectives, and to define “80% basket” generally as investments that are invested in accordance with the investment focus that a fund’s name suggests (“names rule amendments”). See rule 35d-1(g) under the Investment Company Act. During recent Congressional testimony, SEC Chair Atkins indicated that the Commission is in the process of reviewing the Names Rule.

[3] See Investment Company Names Form N-PORT Reporting; Extension of Compliance Date, Investment Company Act Release No. 35963 (Feb. 18, 2026) (extending compliance date for Names Rule-related reporting requirements until November 17, 2027 for fund groups with at least $10 billion in net assets, and May 18, 2028 for fund groups with less than $10 billion in net assets).

[4] See Registered Funds Association v. SEC, No. 24-60550 (5th Cir. 2024). These proceedings are currently stayed while the SEC reviews the 2024 amendments and considers potential changes.

[5] See Regulatory Freeze Pending Review (Jan. 20, 2025) [90 FR 8249 (Jan. 28, 2025)].

[6] See Form N-PORT and Form N-CEN Reporting; Guidance on Open-End Fund Liquidity Risk Management Programs; Delay of Effective and Compliance Dates, Investment Company Act Release No. 35538 (Apr. 16, 2025) [90 FR 16812 (Apr. 22, 2025)]; Investment Company Names, Extension of Compliance Date, Investment Company Act Release No. 35500 (Mar. 14, 2025) [90 FR 13076 (Mar. 20, 2025)]. Pursuant to these extensions, the compliance date for the 2024 amendments is November 17, 2027, for larger entities and May 18, 2028, for smaller entities. The compliance dates for the 2023 amendments relating to the Names Rule, were set to occur this year (June 11, 2026, for funds with more than $1 billion in net assets, and December 11, 2026 for smaller funds). However, as noted above, those dates have now been further extended.